Wavelet routine for multiple cross-regression

wave.multiple.cross.regression.RdProduces an estimate of the multiscale multiple cross-regression (as defined below).

wave.multiple.cross.regression(xx, lag.max=NULL, p = .975, ymaxr=NULL)

Arguments

| xx | A list of \(n\) (multiscaled) time series, usually the outcomes of dwt or modwt, i.e. xx <- list(v1.modwt.bw, v2.modwt.bw, v3.modwt.bw) |

|---|---|

| lag.max | maximum lag (and lead). If not set, it defaults to half the square root of the length of the original series. |

| p | one minus the two-sided p-value for the confidence interval, i.e. the cdf value. |

| ymaxr | index number of the variable whose correlation is calculated against a linear combination of the rest, otherwise at each wavelet level wmc chooses the one maximizing the multiple correlation. |

Details

The routine calculates one single set of wavelet multiple cross-regressions out of \(n\) variables that can be plotted as one single set of graphs (one per wavelet level).

Value

List of four elements:

List of three elements:

List of seven elements:

numeric vector giving, at each wavelet level, the index number of the variable whose correlation is calculated against a linear combination of the rest. By default, wmcr chooses at each wavelet level the variable maximizing the multiple correlation.

dataframe (rows = #levels, cols = #regressors) of original data.

References

Fernández-Macho, J., 2018. Time-localized wavelet multiple regression and correlation, Physica A: Statistical Mechanics, vol. 490, p. 1226--1238. <DOI:10.1016/j.physa.2017.11.050>

Note

Needs waveslim package to calculate dwt or modwt coefficients as inputs to the routine (also for data in the example).

Examples

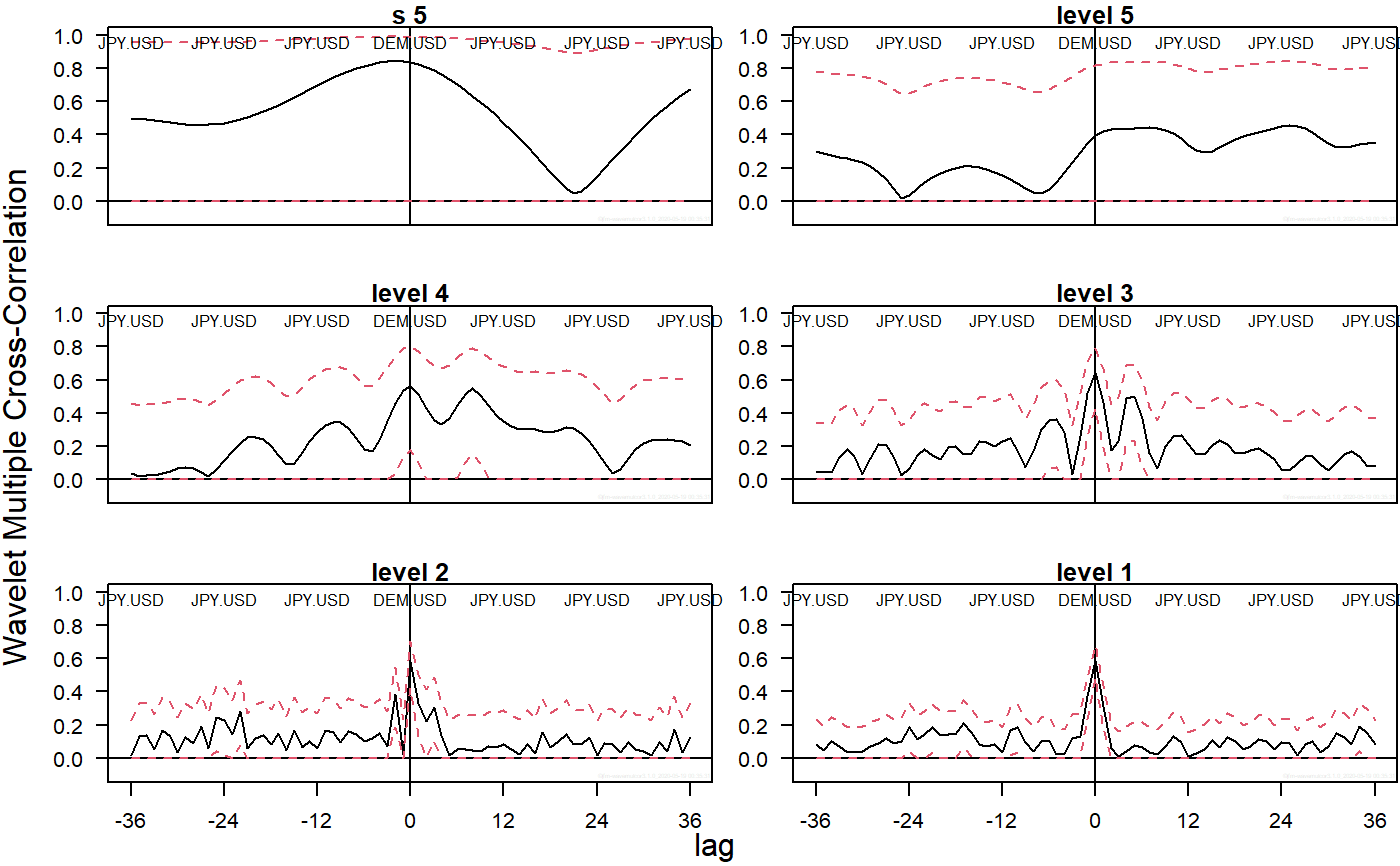

## Based on data from Figure 7.9 in Gencay, Selcuk and Whitcher (2001) ## plus one random series. library(wavemulcor) data(exchange) returns <- diff(log(exchange)) returns <- ts(returns, start=1970, freq=12) N <- dim(returns)[1] wf <- "d4" J <- trunc(log2(N))-3 lmax <- 36 set.seed(140859) demusd.modwt <- brick.wall(modwt(returns[,"DEM.USD"], wf, J), wf) jpyusd.modwt <- brick.wall(modwt(returns[,"JPY.USD"], wf, J), wf) rand.modwt <- brick.wall(modwt(rnorm(length(returns[,"DEM.USD"])), wf, J), wf) # --------------------------- xx <- list(demusd.modwt, jpyusd.modwt, rand.modwt) names(xx) <- c("DEM.USD","JPY.USD","rand") Lst <- wave.multiple.cross.regression(xx, lmax) # --------------------------- ##Producing correlation plot plot_wave.multiple.cross.correlation(Lst, lmax) #, by=2)#> NULL#> Error in plot_wave.multiple.cross.regression(Lst, lmax): object 'J' not found